Download the latest Value Added Tax Return Form for 2026! In-depth guidance on VAT declaration strategies applicable to FDI enterprises. In particular, this article by KMC also provides detailed analysis and professional assessments to help FDI enterprises optimize cash flow and protect profits.

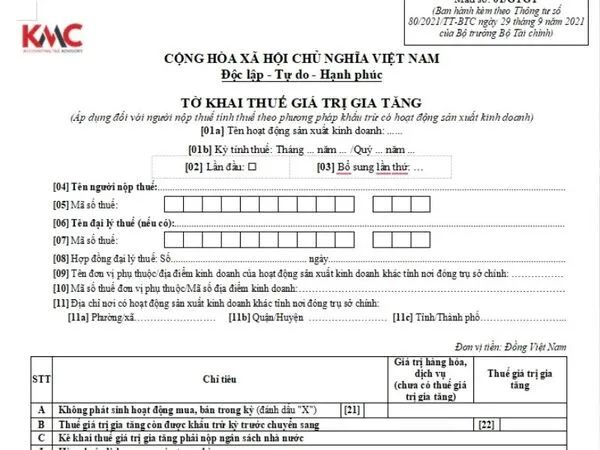

Latest Value Added Tax Declaration Form – Form 01/GTGT

The latest GTGT tax declaration currently applies Form 01/GTGT issued under Appendix II of Circular 80/2021/TT-BTC, applicable to organizations and individuals subject to tax calculation under the credit method and engaged in production and business activities during the tax period (monthly/quarterly).

Download the latest GTGT Tax Declaration Form 01 HERE!

Regulations on Value Added Tax Declaration Forms

Deadline for Submission of GTGT Tax Declarations

Enterprises submitting GTGT tax declarations on a monthly or quarterly basis are subject to different submission deadlines, specifically:

- Deadline for monthly GTGT tax declaration submission: No later than the 20th day of the following month

- Deadline for quarterly GTGT tax declaration submission: No later than the last day of the first month of the following quarter

Penalties for Late Submission of GTGT Tax Declarations

Pursuant to Article 13 of Decree 125/2020/ND-CP, as amended and supplemented by Decree 310/2025/ND-CP, the penalties for late submission of GTGT tax declarations are stipulated as follows:

Level of Violation (Late Submission Period) | Monetary Penalty (VND) | Conditions / Special Notes | Remedial Measures |

1 – 5 days | Warning | Mitigating circumstances required | May be required to pay late payment interest if resulting in late tax payment |

1 – 30 days | 2.000.000 – 5.000.000 | Except cases eligible for warning above | Full payment of late payment interest (if resulting in late tax payment) |

31 – 60 days | 5.000.000 – 8.000.000 | – | Full payment of late payment interest (if resulting in late tax payment) |

61 – 90 days | 8.000.000 – 15.000.000 | – | Full payment of late payment interest (if resulting in late tax payment) |

From 91 days onwards | 8.000.000 – 15.000.000 | No tax liability arises | Full payment of late payment interest (if resulting in late tax payment) |

Failure to submit tax declaration | 8.000.000 – 15.000.000 | No tax liability arises | Submission of tax declaration dossier required |

Failure to submit related-party transaction appendix | 8.000.000 – 15.000.000 | Attached to Corporate Income Tax finalization dossier | Mandatory submission of appendix |

Overdue beyond 90 days | 15.000.000 – 25.000.000 | Tax liability arises + tax and late payment interest fully paid before tax authority announces inspection/audit or issues inspection record | Full payment of late payment interest (if resulting in late tax payment) |

Special case (Clause 5) | Equal to tax payable amount (or total tax of periods), but not lower than average of Clause 4 (approx. 11,500,000) | Applied when Clause 5 penalty exceeds tax payable stated in the tax return | – |

Notes:

- In addition to penalties for late submission of tax declarations, most cases are also subject to late payment interest on tax (0.03% per day on the overdue tax amount).

- If the taxpayer has fully paid the tax and late payment interest before being detected by or before the tax authority issues an inspection record, a lighter penalty level (Clause 5) may be applied.

VAT (GTGT) Declaration – Strategic Analysis for FDI Enterprises

Selection of Declaration Method & Financial Impact

When understanding Value Added Tax (GTGT) declarations, chief accountants and FDI business owners must also pay special attention to the VAT declaration method. The choice of VAT declaration method (credit method or direct method) not only affects the amount of tax payable in the short term but also has long-term impacts on cost structure, pricing, and competitiveness.

- Credit method: Suitable for most large-scale FDI enterprises with high revenue. The advantage is that input VAT is deductible, directly reducing the tax payable and thereby improving cash flow. However, it requires strict compliance with invoices and supporting documents, as well as a more complex accounting system. Any error in input VAT deduction may result in tax reassessment and significant penalties.

- Direct method: Typically applied to small and micro enterprises or certain specific industries. Tax payable is calculated directly based on revenue, which is simpler in terms of procedures but may result in a higher tax burden if the applied percentage rate is high or if the enterprise has significant input costs.

Special Cases and Handling Approaches

For special cases, enterprises may consider the following handling guidance:

- Supplementary and adjusted declarations: When errors are detected, filing an adjusted declaration is necessary. However, attention must be paid to the timing of adjustment, as it may affect the tax period and generate late payment interest. A risk analysis report prior to adjustment is essential.

- VAT refund cases: This is an important mechanism to significantly improve cash flow for FDI enterprises, especially newly established companies, large investment projects, or export-oriented businesses. VAT refund procedures require complete documentation and typically involve a lengthy verification process.

- Handling errors on HTKK software or the e-tax portal: Technical issues such as failure of digital signature connection, file format errors, or mismatches between tax returns and invoices must be resolved promptly to ensure submission deadlines are met. Having a knowledgeable partner such as KMC support can significantly reduce these risks.

Trends and Digitalization Roadmap for 2026

In 2026, e-government development in the tax sector continues to grow strongly. The trend toward full digitalization—from e-invoices, electronic tax declaration to online tax payment—is becoming mandatory. FDI enterprises, with advanced management systems, should leverage this trend to automate processes, minimize manual errors, and obtain real-time reporting data to support financial decision-making.

KMC – Specialized Tax Advisory & Comprehensive Solutions for FDI Enterprises

VAT declaration is not a complicated task, the key point is that all tax and accounting obligations must be properly and accurately fulfilled from the very beginning. This is also one of the major challenges for FDI enterprises when expanding their business in Vietnam. To provide optimal support for FDI enterprises, KMC has been delivering professional and comprehensive tax and accounting solutions, ranging from legal advisory services, performing tax and accounting operations on behalf of enterprises, handling arising issues, to directly working with tax authorities when required. KMC not only provides tax accounting services but also offers integrated ERP system consulting with Vietnam’s tax declaration platforms, helping Japanese enterprises and other FDI companies operate smoothly, efficiently, and in full compliance with regulations. KMC helps you turn compliance obligations into opportunities for financial optimization. For immediate consultation with experts, please contact the hotline: 081 489 4789.