If you are an FDI enterprise, you need to be aware not only of corporate income tax but also of special income tax. So what is it? Why do you need to know it? Which of the following subjects are subject to special income tax? Let’s explore the issue and solutions with KMC in this article.

What Is Special Income Tax?

Unlike Corporate Income Tax (CIT), which is levied on total profits, Special Income Tax is a direct tax that applies only to certain specific industries as prescribed by the State, including petroleum, casino operations, and rare natural resources. This tax is typically calculated based on revenue or profit generated from these specific activities. Any error in determining this tax obligation may lead to serious consequences such as tax assessments, penalties for non-compliance, and long-term reputational damage.

Which Groups Are Subject to Special Income Tax?

Based on the Law on Corporate Income Tax and its implementing guidance documents, taxpayers subject to Special Income Tax (SIT) in Vietnam can be classified into four main groups:

Oil and Gas Exploration and Production Enterprises

Special Income Tax in the petroleum sector is not applied at a fixed rate. Instead, it is negotiated and specifically agreed upon in each Production Sharing Contract (PSC) or Joint Operating Contract (JOC).

This group is generally subject to the highest tax rates, ranging from 32% to 50%, depending on location, project scale, reserve size, and the economic–technical conditions of the project.

Multinational energy corporations should pay particular attention to tax provisions, product-sharing arrangements, and profit distribution terms in contracts signed with Vietnamese partners.

Enterprises Engaged in Exploration and Extraction of Rare Natural Resources

This group includes enterprises operating in the extraction of high-value minerals such as gold, platinum, gemstones, tin, tungsten, and antimony.

According to regulations, the SIT rate applicable to these activities is also very high, typically ranging from 40% to 50%. However, the exact rate may vary depending on the type of resource, mining location, and specific provisions under specialized mineral laws.

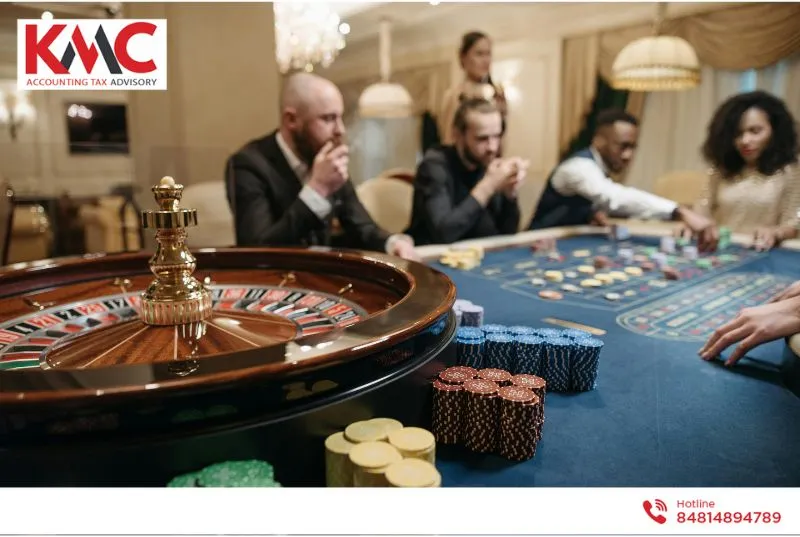

Casino and Prized Electronic Gaming Service Enterprises

In the gaming and entertainment sector, taxable services include:

● Casino business activities (currently piloted only for foreign customers in certain locations).

● Prized electronic gaming services such as jackpot machines, slot machines, video poker, and similar games.

The tax rate is applied to total revenue generated from these services, typically ranging from 30% to 35%.

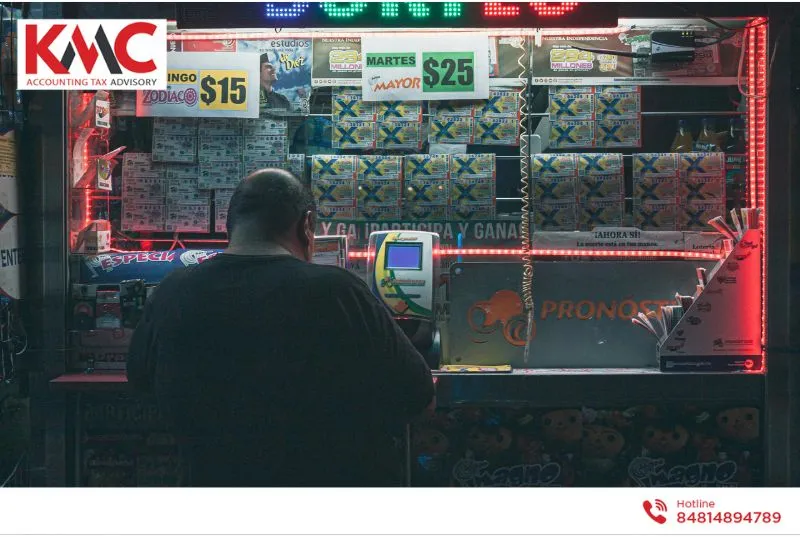

Lottery Business Enterprises

Lottery operations (including traditional and computer-based lottery) are also subject to Special Income Tax.

For this sector, the tax calculation method is specific and is generally based on revenue from ticket sales after deducting prize payouts to winning customers.

Due to its sensitive nature, this activity is typically operated by state-owned enterprises or organizations granted special government licenses.

Note:

In addition to the four main groups above, certain specialized laws may also provide additional regulations on Special Income Tax for other specific activities or types of income.

4 Effective Steps to Manage Special Income Tax Risk

Continuous review and assessment

FDI enterprises, especially multinational groups with complex business structures, may face exposure to Special Income Tax (SIT) in various situations. A manufacturing automobile company (not subject to SIT) may:

● Invest capital in a mineral exploration joint venture (subject to SIT).

● Receive income from the transfer of part of a resource-related project.

● Expand into a new business line without recognizing that it falls under a “special” sector.

Therefore, enterprises should periodically review their entire business structure, business lines, investment projects, and current and potential income sources to timely identify activities that may give rise to SIT obligations.

Separate accounting treatment

For multi-sector enterprises, it is necessary to maintain separate accounting records for SIT-subject activities to ensure accurate tax declaration and finalization.

Proactive policy updates

Tax regulations are subject to change. Therefore, the internal legal department should continuously monitor and update the latest regulations. If you work with a professional advisory firm such as KMC, we will proactively update and adjust in a timely manner.

Complete tax documentation preparation

Enterprises should systematically maintain full documentation and records related to SIT to be ready for any tax audits or inspections by tax authorities.

Finally, the most optimal and sustainable solution for FDI enterprises is to cooperate with a trusted legal and tax advisory partner that has deep expertise in both Vietnamese legal systems and international business culture, such as KMC. We do not only answer the question “which groups are subject to Special Income Tax?”, but also accompany you in building a comprehensive tax advisory, optimizing financial obligations, and ensuring the safety and long-term sustainability of your investment activities in Vietnam.