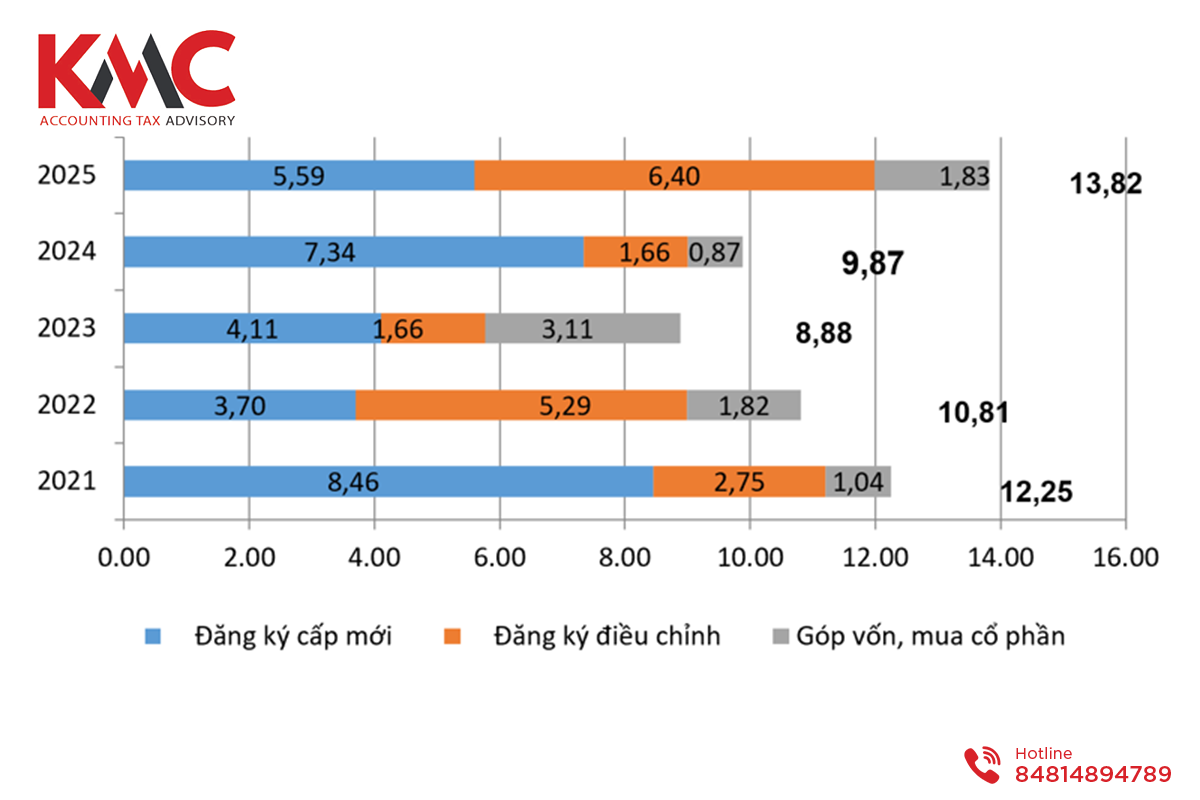

According to statistics, as of April 30, 2025, the number of foreign-invested enterprises (FIEs) in Vietnam appears to be the highest in the past five years. The total registered foreign direct investment (FDI) capital at the Departments of Planning and Investment across provinces and cities has also increased. To create competitive advantages in attracting more FDI and to elevate Vietnam’s position within the region, the government has gradually developed and enhanced transparency in investment attraction mechanisms. Among these measures is the compliance framework governing the remittance of profits to parent companies by FDI enterprises, which must be properly conducted in accordance with applicable legal regulations.

Source: vneconomy

This article provides important information regarding the remittance of profits to parent companies, based on the guidance from the General Department of Taxation as stated in Official Letter No. 4480/TCT-CS dated October 10, 2023, for your reference. This article is not intended to provide legal or tax advice to any individual or organization. Please contact KMC using the information below, or consult with tax professionals for detailed guidance.

Methods of Remitting Profits to Parent Companies Outside Vietnam

As of now, there are a total of four methods for remitting profits to parent companies located outside of Vietnam. These include: dividend distribution; service fee collection under service contracts; internal borrowing and lending; and transfer pricing. Let’s take a closer look at some key information related to these methods.

Dividend Distribution

This refers to the distribution of after-tax profits to the parent company once the subsidiary meets the conditions for dividend distribution as stipulated by law. According to the current Enterprise Law, the eligibility to distribute dividends means the enterprise has fulfilled its tax obligations and other financial liabilities. Dividend payments are conducted by enterprises operating in the form of joint-stock companies.

The dividend distribution process must also comply with the company’s charter and relevant regulations. For example, dividends can only be distributed after the FDI company in Vietnam completes the Corporate Income Tax (CIT) finalization, establishes reserve funds, and holds a General Meeting of Shareholders to approve the dividend distribution decision. Dividends may be remitted in cash or assets.

The parent company may be exempt from tax if certain conditions are met.

Service Fee Collection under Service Contracts

Some foreign-invested enterprises (FIEs), for the purpose of operating their business in Vietnam in alignment with their corporate group or parent company’s system, require consulting, system usage, and other related activities connecting the subsidiary and the parent company. Typically, these enterprises enter into service contracts to collect such fees.

For this type of arrangement, enterprises need to ensure that the contracts are executed with reasonable costs and are supported by complete invoices and documentation in accordance with tax laws and other relevant regulations. Additionally, care must be taken to avoid violations of transfer pricing regulations if the transactions involve related parties.

Internal Borrowing and Lending

Borrowing and lending to facilitate investment activities in Vietnam is also a common method used by foreign-invested enterprises (FIEs). In this case, loan agreements must comply with applicable legal regulations.

Transfer Pricing

Transfer pricing is generally understood as the practice of setting and applying pricing policies for goods, services, and assets transferred between related companies at prices that do not reflect market value, with the intention of minimizing tax liabilities payable to the tax authorities. This practice is strictly prohibited and considered a violation of the law.

Therefore, related-party transactions between affiliated entities must comply with current legal regulations. You may refer to provisions in the Tax Administration Law and other relevant legislation for further guidance. It is highly recommended to seek advice from experts on this matter before engaging in any such transactions.

Profit Remittance Abroad

Profits remitted abroad must be legitimate profits earned from direct investment activities in Vietnam in accordance with the applicable investment laws.

Such profits may be transferred in cash or in kind. Compliance with foreign exchange regulations and tax laws is required.

Timing for Remitting Profits Abroad

By law, profit remittance abroad can be conducted annually after the foreign-invested enterprise (FIE) has fulfilled its financial obligations to the Vietnamese government in accordance with current regulations. Additionally, the enterprise must have completed the submission of audited financial statements and the corporate income tax (CIT) finalization declaration for the fiscal year to the competent tax authority.

When the FIE completes its project and no longer intends to continue investing, this is also a permitted time to remit profits to the parent company. The procedures and documentation required remain consistent with the processes previously mentioned.

Notification of Profit Remittance Abroad

The notification of profit remittance abroad is considered a mandatory step for foreign investors. Foreign investors may either submit the notification online themselves or authorize the FDI enterprises in which they have invested to carry out this notification on their behalf.

The notification must be sent to the competent tax authority at least 7 days prior to the expected date of profit remittance to the parent company.

Confirmation of Tax Obligation Fulfillment

In cases where a foreign contractor does not directly declare and pay taxes to the tax authorities, this responsibility is performed by the Vietnamese enterprise through withholding and remittance on behalf of the foreign contractor. The Vietnamese enterprise must submit a written request for confirmation of tax obligations fulfillment with the state budget to the competent tax authority managing the enterprise.

This regulation is stipulated in Article 70 of Circular No. 80/2021/TT-BTC dated September 29, 2021.

KMC – Your Trusted Business Advisory Partner

KMC is a consulting firm established in 2008 by Japanese and Vietnamese experts. With many years of experience and a diverse client portfolio, KMC offers advisory services in tax, corporate matters, transfer pricing, and other related services.

Please contact us whenever you need assistance.

Hotline: +84 81 489 4789