On 19 October 2020, the Government issued Decree 126/2020/ND-CP (“Decree 126”) detailing several articles of Law on Tax Administration. Decree 126 comes into force from December 5, 2020.

Decree 126 consists of 9 chapters and 44 articles. This decree comes into force from 05 December 2020 subject to some transitional rules.

Highlighted points in Decree 126 are as follows:

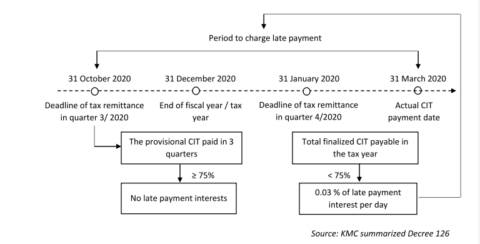

- According to article 8, Decree 126, total corporate income tax (“CIT”) paid in the first three quarters of the tax year must not be less than 75% of the finalized CIT payable. In case, the paid tax in three quarters is less than 75%, the fine of late tax payment will be applied for the retrospective amount from the deadline of tax remittance in the 3rd quarter to payment date to the State Budget.

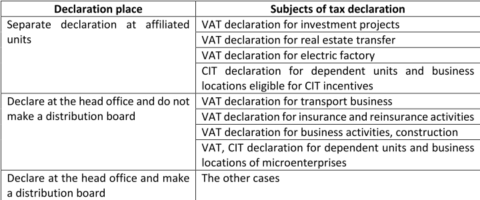

- Article 11 further clarifies the tax declaration regulations for dependent units. Taxpayer does concentrated accounting at the head office and has dependent unit in other provinces, the taxpayer shall declare tax at the head office and distribute the payable tax amount in each provice.

Some special cases about the place to be declared value added tax (“VAT”), mentioned in the table below:

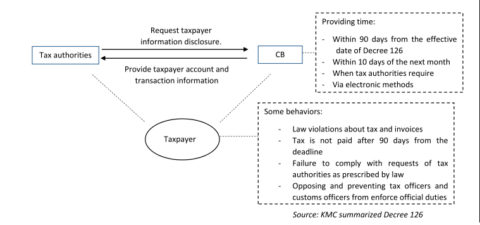

- Articles 29 and 30 of Decree 126 provide for the duties and responsibilities of disclosing taxpayer information of commercial banks (“CB”).

- In addition, according to Article 14, Decree 126 expands the tax authorities’ right to tax liability imposition in some specific cases:

+ Companies that enter into method of determining tax price agreements do not comply with commercial principles to avoid taxes.

+ Using illegal invoices and using invoices illegally but goods and services in transaction are real to declare tax.

+ Failure to comply with inspection decisions within 10 days and tax inspection within 15 days.

+ Failure to comply with the regulations on determination and transfer pricing declaration.